Thank you for your answer.

I think, current tokenimics needs one more guide through. Articles from medium feels old.

Thank you for your answer.

I think, current tokenimics needs one more guide through. Articles from medium feels old.

Happy to help. Luckly I spent time to deep dive in what we used to have and there is no time cost for me to refresh it.

The thing which really annoying imo is that while we are voting for/against the PI, the main convo here is the change of the tokenomics, not the index discussion. And as I see the token distribution schedule (both - old and new) is something the most part of the community (even the active ones) are not familiar with

Let me comment on the key parts of the proposal separately

Tokenomics:

why the token distribution schedule proposed by @YanDelphi is an elegant solution and better than the previous token distribution schedule

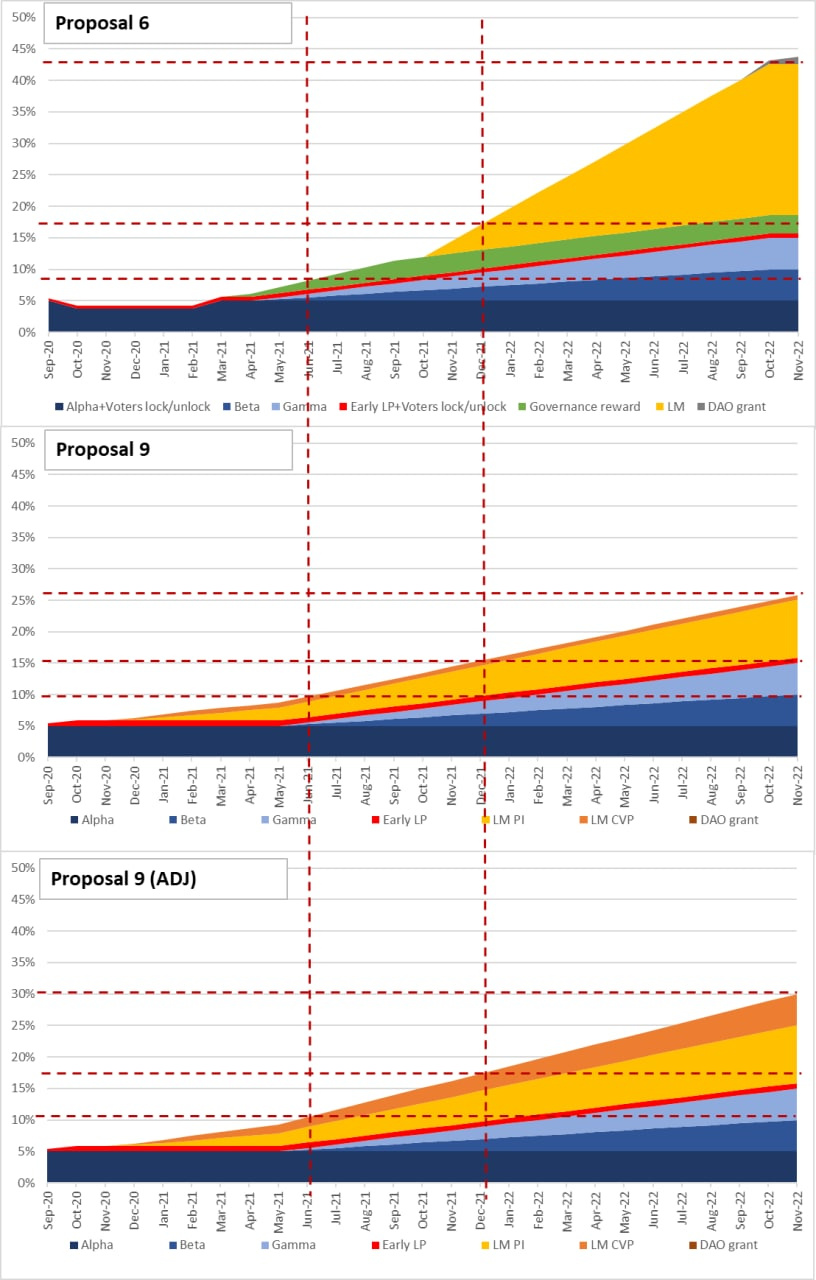

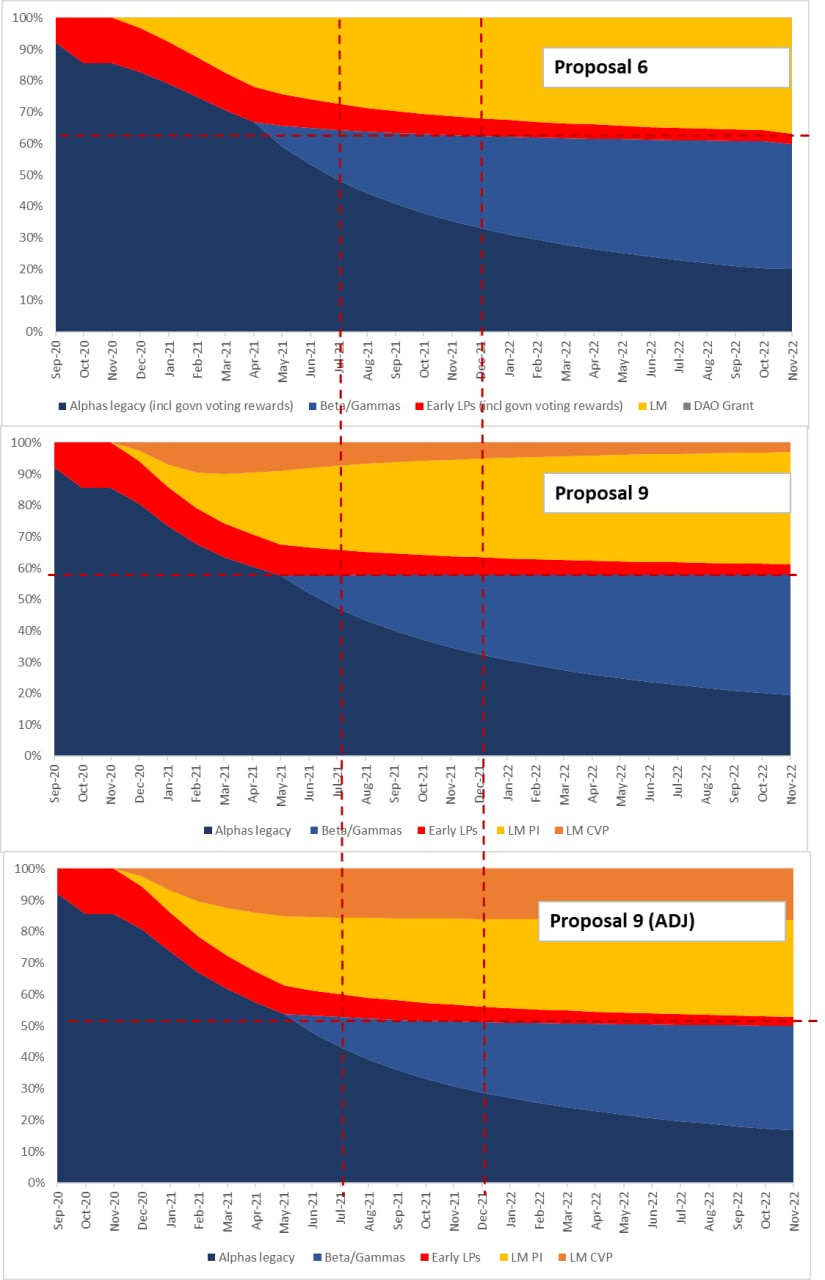

Lets compare what did we have and what is proposed - token distribution schedule / testers voting power dilution (see the charts below)

a. CIRC SUPPLY: a way better distribution schedule - by YE2022 the circ supply is 30-40% less!..

Proposal 6: 8% - 17% - 43% / 1H2021 - YE2021 - YE2022 respectively

Proposal 9 / 9 (ADJ): 10-11% - 15-18% - 26-30% / 1H2021 - YE2021 - YE2022 respectively

b. Testers voting power dillution: while the testers voting power is even more diluted!

Proposal 6: 63% of votes belong to the testers by YE2021

Proposal 9 / 9 (ADJ): 52-58% of votes belong to the testers by YE2021

Conclusion: Great proposal overall! Please see a couple of adjustment from my side below

SUGGESTIONS:

In case we change the tokenomics anyway lets add the idle tokens burn as @CryptoSignalz suggested in Proposal 8 Proposal 8: Reduce diluted valuation by burning part of the community treasury.

I would suggest burning of 25% of TTS and then decide whether we need to burn more tokens, while consider using the remaining locked “idle” 25 mn CVP as a protection from a hostile take over (please see here CEXes, government and interests

the discussion initiated by @Zero)

Happy we got back to keeping the CVP/ETH pool - I have been arguing to keep it all the time.

You guys say its important to have the liquidity there and still assume that the rewards will be excluded since Jan-2021 - so what will happen with the CVP/ETH liquidity (please see the current example of UNI)

Lets just consider in the base case model that the rewards will be halved since Feb-2021 (40.5k CVP per week) - this is more realistic

I’m for merging proposal 8 with proposal 9 and burn 25% of TTS.

If we plan to burn a portion of the TTS in the near future it is better to include it in the current tokenomics change rather than frequent changes which broadcast uncertainty.

BTW, How about putting it in the following way:

Include a statement that by the mid of December-2020 we will either burn or lock up for at least 3 years up to 50% of TTS

Now to the next part

Power Index

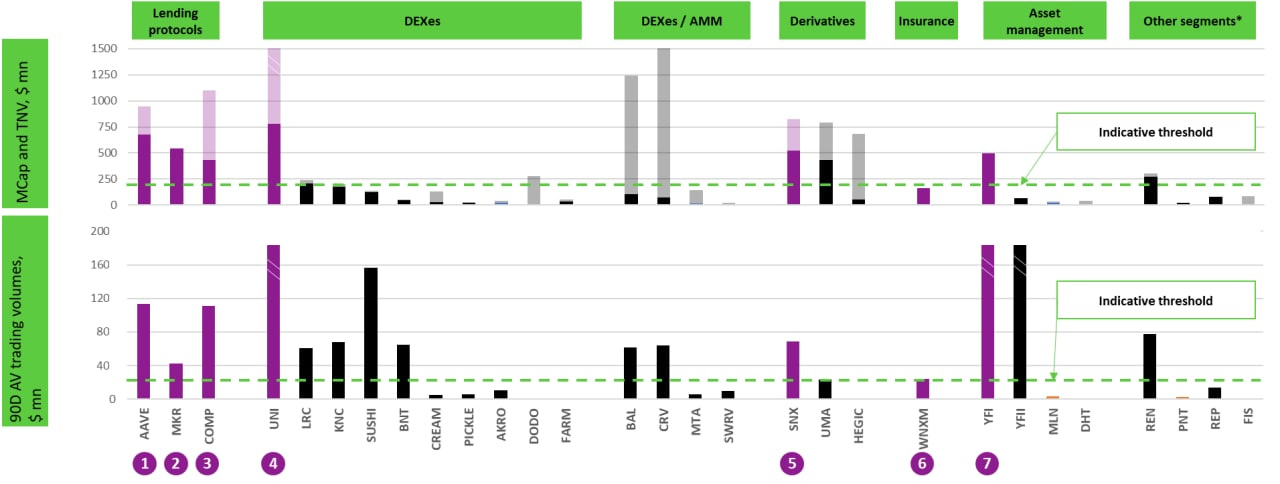

Wanted to provide a supporting analysis from my side - “why these projects?”, hope it will help the community to vote

As DeFi meta-governance ETF, PI has exposure to all the key segments of DeFi, while the initial PI composition is skewed towards the basic and most resilient layer - Lending protocols (MKR, AAVE, COMP)

At the same time there are some restrictions for PI composites selection:

a. Significant MCap and ADTV as PI’s composites shares need to be easily adjusted (I roughly estimate this level at ~$200 mn for both Mcap and ~$20 mn ADTV)

b. FDV/Mcap ratio <= 5x to limit the value dilution risk, while keeping recently listed projects with a large number of tokens yet to be unlocked (namely - UNI)

c. Decentralized governance function (GT). This is the reason why such projects as REN, Augur (and Chainlink) are not included

Some other great projects such as BAL and CRV are not included because of the FDV/MCap (+ specific lock up terms for CRV) and also the fact that PI has exposure on DEXes via UNI

Similar reason is why WNXM is included instead of LRC, KNC and Sushi – WNXM is the only way to get exposure on a very promising insurance market, while DEXes are already represented by UNI

Also, FDV and MCAp to TVL ratio is much higher than PI components’ average for LRC and KNC (9-18x vs 0.5-1.5x)

So the only project with relatively weaker metrics included into PI is wNXM.

But, I believe, we need take several facts into account:

Thanks for a so visual comparison @Sergey, can you please clarify on what do you mean by “Idle token”?

50 mn CVPs that will be locked at least for the next 3yrs - burn half of them and use another half as a veto voting mechnism in emergency case

Centralisation? Yes

Elegant? yes:)

To be honest, I don’t truly understand what all you say but great to see an active proposal here.

aahhaha why?

this explains pretty simply why the proposed tokenomics is beter

And this gives more details on the selection of PI composites

Great, thank you so much

Hey everyone, added two modifications to the proposal that I believe will definitely improve it.

read the proposal. I like this improvement - it will massively boost APY and TVL, and will help to compete with PieDAO/DPI. Balancer 80/20 is also a good option for PIPT

There’s something really major I think someone needs to clearly state/confirm: Am I correct to think that the liquidity mining reward of 400k/mth is only referring to the provision of liqudity for CVP/ETH in Uniswap/Balancer (yellow bit in the graph in the proposal). There is a seperate liqudity incentive (white bit in the graph in the proposal) for PIPT suppliers (either directly staking PIPT via the powerPool app or via a (currently non-existing) PIPT/ETH Uniswap pool)…Am I getting the proposal right here? If so, how much is the reward for PIPT suppliers?

What is ‘Organic LPs (community pool?)’?

What is DAO grant?

Do current incentives for liquidity provision of CVP/ETH on Uniswap come from ‘Organic LPs (community pool?)’? Do they come from the 77m in the Treasury?

you also say:

“so 24 000 000 LM rewards

and 3 000 000 govn rewards

and 4 500 000 community pool

were sitting inside that 77 000 000”

Where can I see the breakdown of how the 77m is earmarked? You covered 31.5 of 77m…

why rush the burning/locking up by Dec 20? Why not let the project grow for a few months and then vote again on burning/locking up?

FOR both the adjustments

All is correct. Mate all the numbers are in the proposal (yet ot be finalised though)

Well, just not to constantly change the tokenomics: we can include all the key adjustments into one proposal IMO

Hey everyone, after discussing with the team we added two more minor modifications to the proposal.