Three Items included in this vote:

-

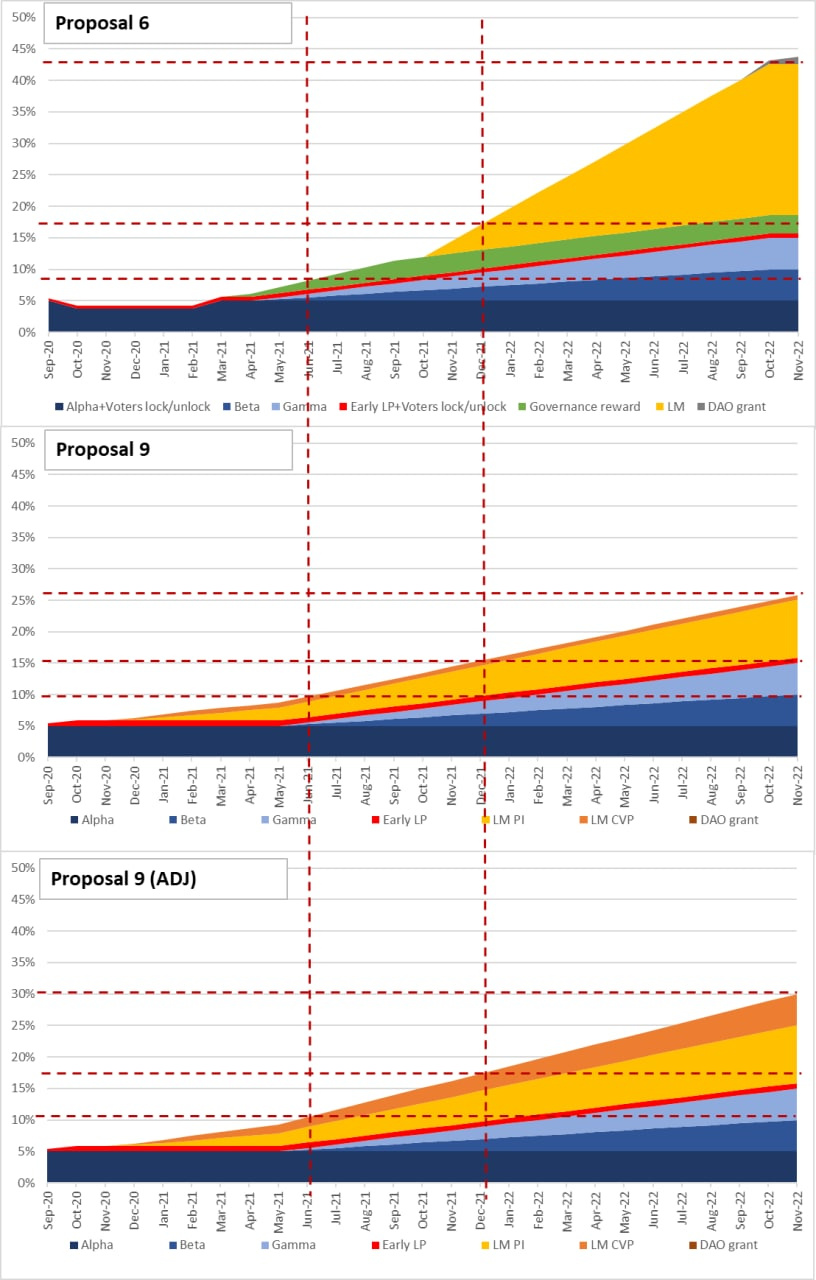

The composition of the index will remain relatively unchanged in the transition, consisting of CVP, YFI, SNX, LEND, wNXM, UNI, COMP, and MKR. The only change will be AAVE replacing LEND now that Aave has gone through the token migration. Since the index remains unchanged, the 3M in CVP rewards will also no longer be rewarded for those who vote on the composition.

-

Liquidity Mining Program for Power Index

Previous: The previous plan was to provide 2M CVP in monthly rewards to Index Liquidity providers, with the rewards being locked for one year.

New Proposal: The new proposal is to change this rewards program to 400k CVP per month, with 50% of the reward vesting immediately while the other half vests over the following 10 weeks.

- Liquidity Mining Rewards for CVP

Previous: There are currently multiple pools, ranging from a 50-50 ETH/CVP pool on Uniswap to 95-5 CVP/ETH Balancer pool, that are being rewarded with liquidity incentives. This has fractionalized liquidity a bit, resulting in a dex market that’s less liquid than it should be.

New Proposal: We propose to shift all rewards to the 50/50 Uniswap pool. Specifically, this pool would receive 91,000 CVP on a weekly basis, and those rewards would come with a 10-week vesting period. This will enable those who want to speculate to receive sizable returns without creating a supply glut from rewards

Rationale:

It’s time for the main Power Index to launch. The purpose of this proposal is to create a smooth transition from the current baby index to the main index, while incorporating a few improvements to the liquidity mining program. The composition of the index will remain relatively unchanged in the transition, consisting of CVP, YFI, SNX, LEND, wNXM, UNI, COMP, and MKR. The only change will be AAVE replacing LEND now that Aave has gone through the token migration. The makeup (assets and weights) can be changed in the future through governance proposals, but will be kept unchanged in the interest of ensuring a smooth initial transition.

There will be a few changes made to the liquidity mining program. To make the changes as digestible as possible, we’ll describe the initial proposal along with the thought process behind the switch.

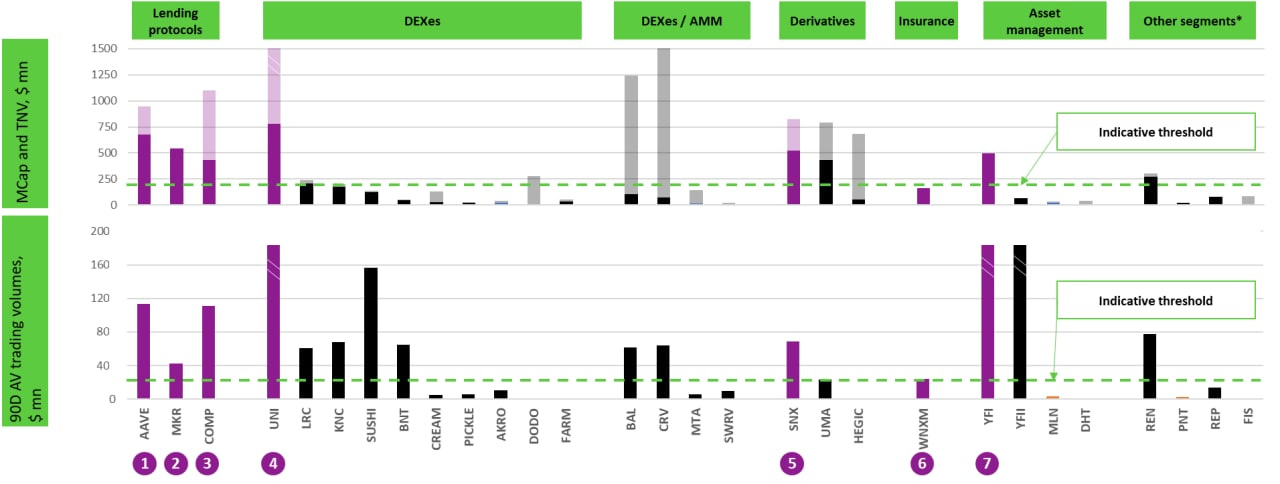

Just to restate the obvious, the goal of this index is to vacuum up as much TVL as possible. As the index grows, it increases its sustainability, governance power, and the fees it can generate from governance activities.

The previous plan was to provide 2M CVP in monthly rewards to Index Liquidity providers, with the rewards being locked for one year. This accomplished the goal of creating additional incentives for users to add liquidity to the index while not substantially increasing the supply of CVP. There was, however, a bit of a mismatch in that users wouldn’t receive these rewards for quite some time, so it diminished the impact the liquidity mining program would have. The rewards had to be fairly substantial in order to compensate for the wait, which is why they were 2m per month.

The current proposal is to change this rewards program to 400k CVP per month, with 50% of the reward vesting immediately while the other half vests over the following 10 weeks. Below you can see what that looks like in terms of yield. We believe these yields are very attractive when considering that it’s in return for holding a basket of highly popular assets.

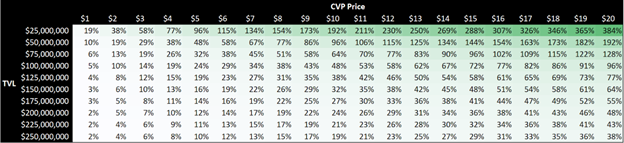

Aside from the quality of assets, the other important aspect of this design is that it’s sustainable. This sustainability is the result of a combination of factors that we’ll discuss. As with most farms, yield increases with token price (because it’s the reward) and decreases with TVL (because the denominator goes up). At the surface, these relationships hold with CVP as well. An important difference maker is that CVP is included in the index and it maintains a fixed weight, meaning that demand for the token scales with TVL in the index. As users deposit capital to farm assets, the value of the CVP in the index must increase as well. CVP’s weight in the index is 12.5%, but it can be increased through governance.

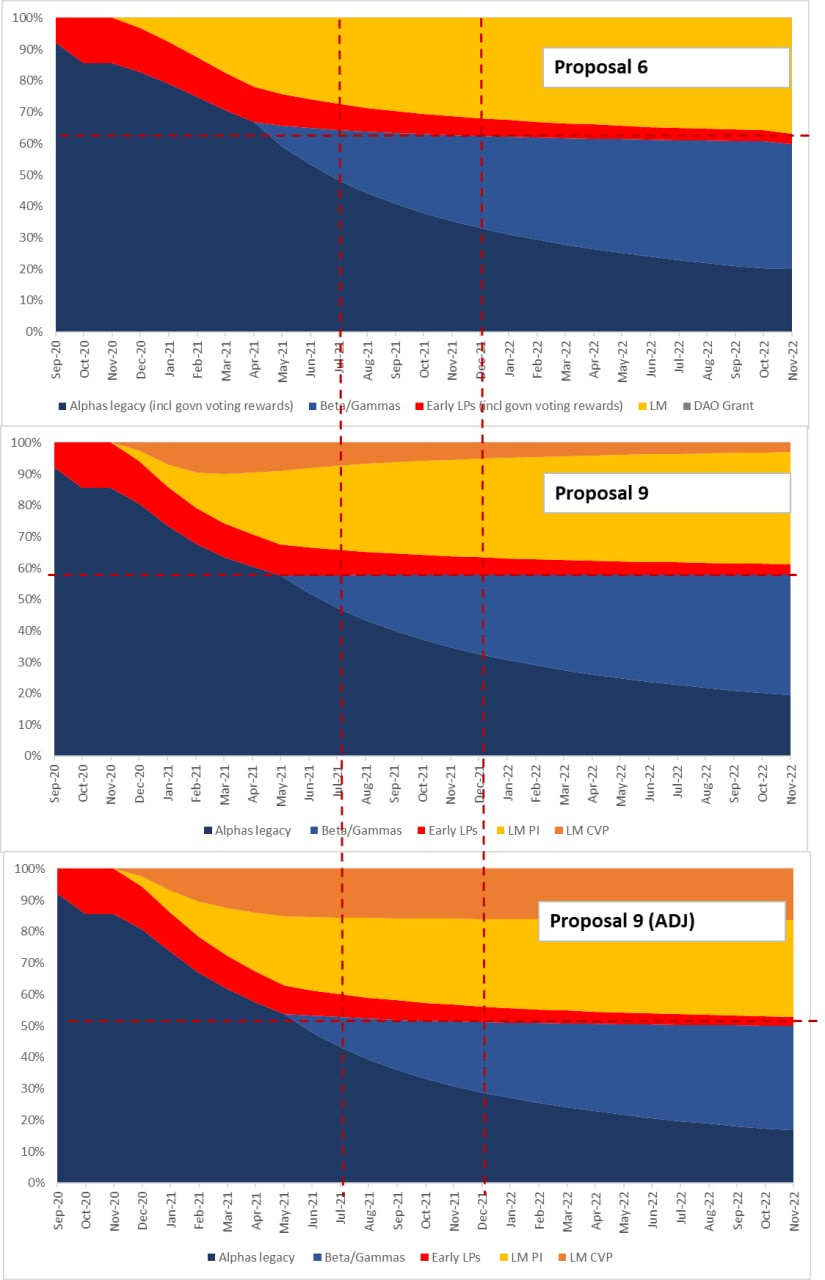

The two primary motivations behind deploying capital in this situation is either to farm CVP with existing blue-chip tokens or to speculate on the price of CVP. There will definitely be users that do both, but the capital will be deployed separately. CVP’s liquidity mining program is already designed to help these individual motivations become mutually beneficial, but we want to strengthen that dynamic. The reason we say it’s mutually beneficial is described in the visual below. Speculation by users leads to an increase in CVP price. This increases the yield on deposited assets, which leads to an increase in TVL as users seek to capture that yield. As TVL scales up, so does the demand for CVP as it needs to maintain its fixed weight in the index. This continues to support price and creates strong positive reflexivity for this index to consume assets.

When referring to CVP in the index, the term we used was ‘value’ of CVP in the index. If there’s $100m of assets in the index, there needs to be $12.5m worth of CVP in it as well. Price on the other hand will be determined by quantity of tokens in that index. This is where the symbiotic relationship between liquidity providers and speculators comes into play, along with our next proposal change.

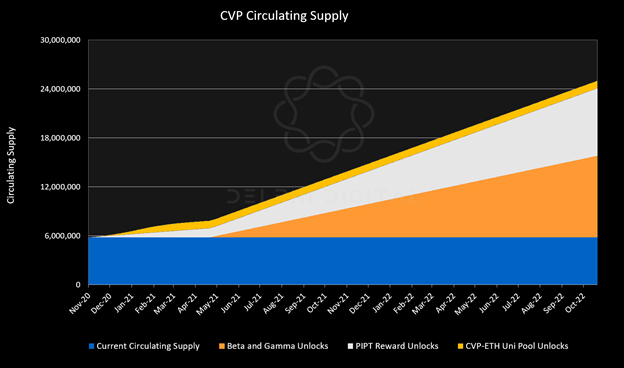

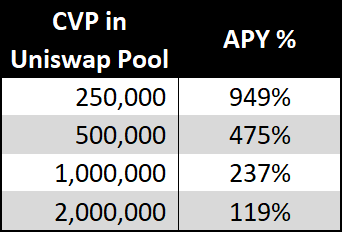

Those who want to speculate will not deposit CVP in the index. They do, however, need a productive way to utilize those assets. There are currently multiple pools, ranging from a 50-50 ETH/CVP pool on Uniswap to 95-5 CVP/ETH Balancer pool, that are being rewarded with liquidity incentives. This has fractionalized liquidity a bit, resulting in a dex market that’s less liquid than it should be. We propose to shift all rewards to the 50/50 Uniswap pool. Specifically, this pool would receive 91,000 CVP on a weekly basis, and those rewards would come with a 10-week vesting period. This will enable those who want to speculate to receive sizable returns without creating a supply glut from rewards. The Uniswap pool will be able to hold over 2 million CVP (and the corresponding quantity of ETH) while still receiving triple APY.

Here’s what the circulating supply schedule would look like assuming the conditions described above, with the liquidity incentive program for the Uniswap pool continuing through the end of January. That’s not to imply it ends in January since governance will dictate all liquidity incentives. The goal here is to show that these rewards will not flood the market with supply.

We’ve also designed a liquidity mining incentive scheme that has impermanent loss insurance built in. It rewards you additional CVP in order to directly offset the impermanent loss that you specifically were exposed to. It’s conditional on providing liquidity for a yet to be determined amount of time. If you withdraw liquidity prematurely then you’re only compensated for a portion of the impermanent loss. The goal here is to incentivize long term liquidity provision and allow individuals to be comfortable providing it. We’ve spoken with the team about it, and it will be formally presented in another proposal shortly after this one.

We believe the current plan should be sufficient for speculators to have the necessary incentives to provide a deep market on Uniswap for CVP, in turn creating productive supply sinks that are net beneficial to all participants. The launch of Powerpool’s Oracle product, along with the recent listing on Binance, will lead to additional supply sinks that should further strengthen the ability of this model.

The final aspect of this proposal is the division of the liquidity incentive rewards for Power Index suppliers. After providing assets to the index, you then stake the LP token representing that liquidity in one of two ways. Users can either directly stake the token and receive the yield, or stake the token in a 50/50 liquidity pool with ETH. The current pool uses USDC, but ETH is positively correlated with the assets in the index which would reduce impermanent loss.

Directly staking the token to receive the yield is the most straightforward way to participate. The reason to create a liquid PIPT/ETH pool is to make it as easy as possible for individuals to add capital to the index. If a user doesn’t feel like adding the assets directly, they can just purchase the index LP token to receive the yield. When PIPT is purchased for exposure, it drives the price up a bit creating an arbitrage situation. Other users can then deposit the underlying assets to create more PIPT tokens that they can sell and close the arb. Enabling users to add assets to the index as easily as possibly is why it’s important to create a liquid PIPT/ETH market. The rewards are divided between these two participants (direct PIPT stakers and PIPT/ETH stakers) with ⅓ going to the former and ⅔ going to the latter. It’s divided this way to ensure both participants receive an equal yield since there would need to be twice as much capital in the PIPT/ETH pool to match the direct PIPT stakers.

We wanted to make 2 modifications to this proposal.

Modification 1:

The first modification is to shift the Power Index reward pool from a 50/50 PI/ETH pool to an 80/20 PI/ETH pool. To recap, Power Index LP’s can claim rewards by either directly depositing their PI LP token in the PowerPool app, or they can deposit it in an AMM with ETH and deposit that LP token on PowerPool.

Technically speaking, the highest reward yield would be achieved if all PI LP tokens were directly deposited without an ETH pair because rewards (numerator) would be given to the smallest pool of capital (denominator). The tradeoff here is that without PI Tokens in an AMM, it removes a very simple way for users to deposit capital into the index. This simple way is one where a user buys the PI LP token from the AMM driving up the price of the token. There’s now an arbitrage opportunity where someone else can come in and supply the underlying assets at a slight discount to the value of the PI token they’d be issued. They would then sell the PI token to close the arb, and we’re left with more assets in the Index than when we started with. This is very similar to the role of an Authorized Participant in the Creation/Redemption mechanics of an ETF.

Now that we’ve addressed why we need PI tokens in an AMM, we can discuss why we should shift the balance from 50/50 to 80/20. When comparing the two, a 50/50 pool has better execution than an 80/20 pool, but also suffers from more impermanent loss. They net out a bit, but we’ll go into further detail about them in a bit. The main reason we want to switch to an 80/20 is because it makes the rewards materially more efficient for the Power Index. In a 50/50 pool you’re effectively paying people for also providing eth liquidity. By reducing ETH’s weight in the pool, more rewards are now being given to Power Index assets.

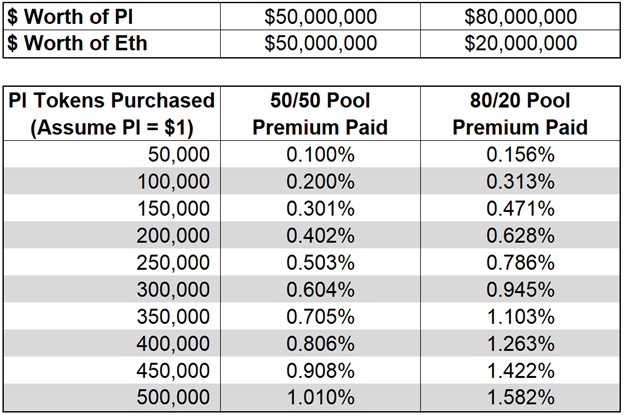

Assuming the 50/50 pool and 80/20 pool hold the same amount of PI, if the yield for the 50/50 pool is x, then the yield for the 80/20 pool is 1.6x. This 1.6 multiplier is especially meaningful when you have triple digit yields. We believe this yield gap gets closed by means of additional PI being deposited, which is a good thing because now these rewards can service more Index Assets. Will provide a quick example below. I wouldn’t focus on the specific $ values of these assets as they’re purely demonstrative.

Above we demonstrate the closing the of the yield gap. Rather than having an 80/20 pool with $50m worth of PI and $12.5m worth of ETH earning 1.6x the yield of a 50/50 pool with $50m in PI and $50m in ETH, we believe the 80/20 pool will increase its asset base to $80m in PI and $20m in ETH. Again, you’re now able to service a lot more capital from the PowerPool Index with the same rewards. The negative aspect of the 80/20 pool we described earlier was the execution. The fact that yields will help normalize cumulative capital by bringing it to $100m is important because it diminishes the impact of the reduced execution quality. Above you can see the relative slippage/premium paid between the two pools for different transaction sizes. If someone wanted to purchase 50k PI tokens at $1 each, the slippage difference is negligible. Even as you begin to size up your order, there is minimal difference in slippage. If you’re making a large purchase from the liquidity pool and the slippage is more than you’d like it to be, you can always break up the order into two or three smaller purchases. Considering this is the only actual downside to going with an 80/20 pool, it seems highly worthwhile. The other benefit of the 80/20 pool we mentioned earlier was that it would have less impermanent loss.

To recap, the benefits of an 80/20 pool are that it would materially increase yield and reduce impermanent loss. The downside is mildly worse execution, quantified above, and easily remedied by dividing the order into smaller purchases.

Modification 2:

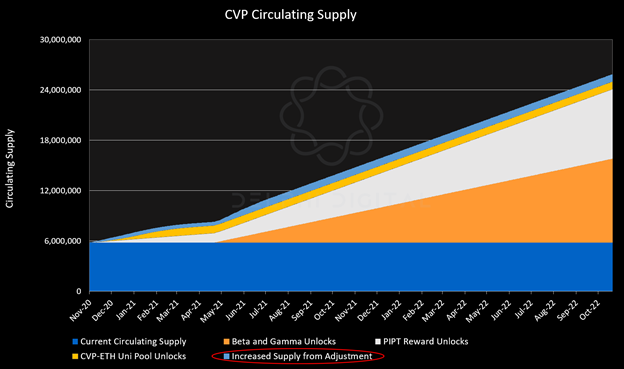

The second modification is to increase the Power Index rewards during months 1 and 2. The current proposal has monthly rewards at 400k CVP for the foreseeable future. We would like to increase rewards to 1M CVP in the first month and 700k CVP in the second month. The purpose of this adjustment is to help kickstart the flywheel described above by incentivizing capital to flow into the index early on through a strong yield. This would create strong demand for CVP since its an equally weighted index, which would continue to bolster index reward yields and drive more capital into the index. We visualize the increase this would lead to in circulating supply below in teal, and it’s clearly negligible. Since it’s in the early days, it also comes at a time when it’s most impactful, making the relative value of this slight increase in supply that much higher.

After discussing with the team, there were two more small adjustments we wanted to make. The first one being a conditional vesting parameter for PowerIndex rewards that’s based on total Index liquidity. We show the specific parameters below.

<$1,000,000 : 10% rewards immediately vest (90% 10 week vest)

From $1m to $5m: 20% immediately vest (80% 10 week vest)

From $5m to $10m: 35% immediately vest (65% 10 week vest)

From $10m: 50% immediately vest (50% 10 week vest, in line with most recent proposal)

The normal rule is that 50% of rewards vest immediately and 50% vest over a 10 week span. Once there is at least $10m of total liquidity in the index, this adjustment has no effect. This means the only difference is when the Index has less than $10m of liquidity. The % that immediately vests is seen above, the with remainder vesting over 10 weeks. The goal here is to reduce the flood of rewards in the early days when the index is starting to grow, and return to the usual schedule once there is enough liquidity in the index to absorb these rewards.

The other small change is to double the CVP/ETH Uniswap LP Rewards in the first month (to 182k CVP per week), but keep the other months unchanged at 91k CVP per week. This is to further supplement the thought process used in adjustment above, where we want to allow the index to grow quickly without having to rapidly absorb CVP rewards. We believe this incentive can absorb CVP and drive value to the token while the Index itself grows. The 10 week vest on CVP/ETH LP rewards will remain.