Motivation:

The foundamental motivation of this proposal is to find ways to increase the useage of the CVP token and increase the value of the powerpool protocol. This token should not be used as farm and dump and the best ways to prevent this is to find different usecases for it.

Suggestion:

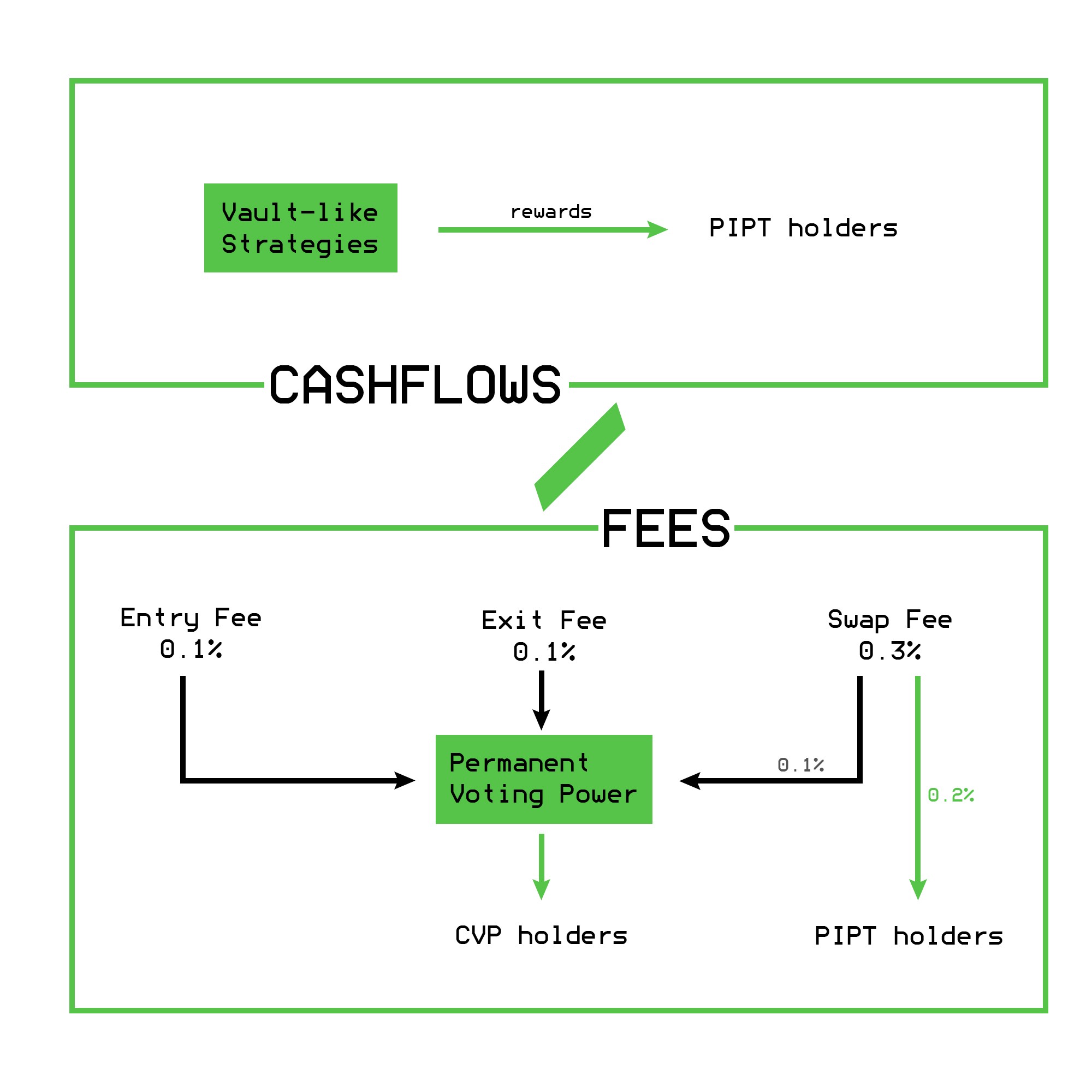

The most interesting reason for speculators/investors are economical reasons. Thats why i suggest that the CVP token should have some kind of cashflow. The PP treasury (0xd132973eaebbd6d7ca7b88e9170f2cca058de430) has already collected about 200k USD in different tokens.

So i suggest the following things to happen:

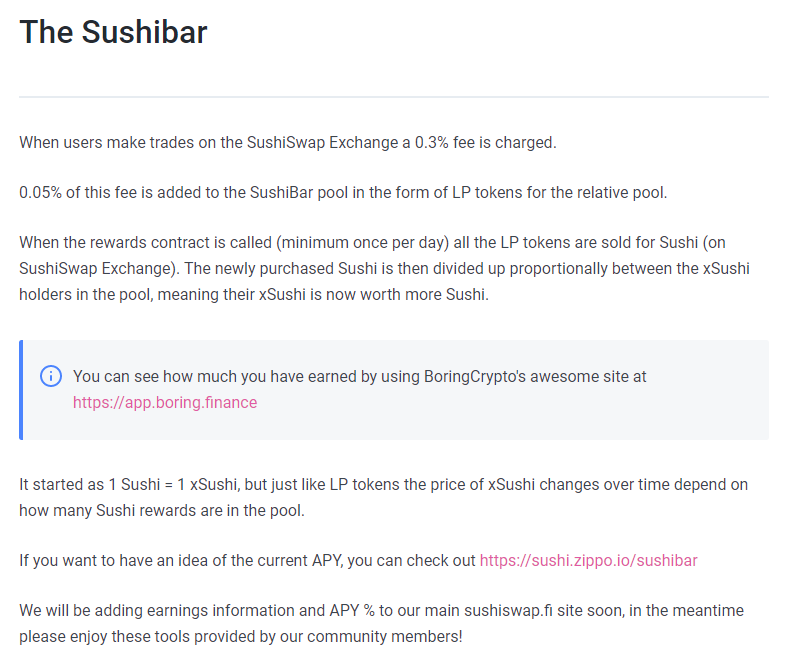

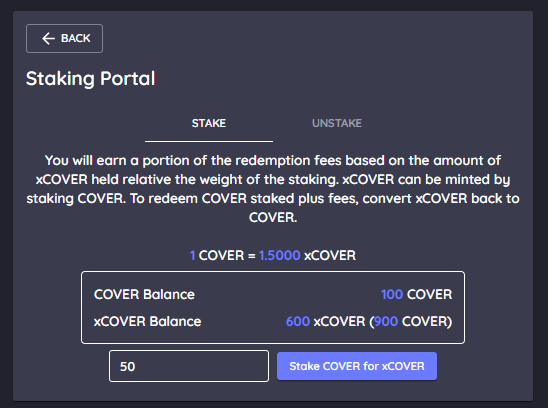

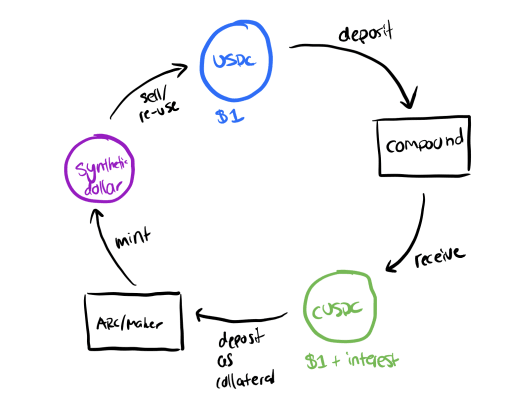

We should implement something like the Sushibar but for CVP: https://docs.sushiswap.fi/products/yield-farming/the-sushibar

With the earned fees CVP should be bought and added to this pool. So that 1 xCVP is always bigger than 1 CVP.

And on top of that i suggest that the vested CVP automatically go into this staking contract (not the earned one, the vested ones you are allowed to claim).

Benefits to the holders and the protocol:

- every interested short or longtime holder will be able to earn an additional cashflow

- because the vested CVP move into the xCVP contract the user does not have to pay any gas fees if he is interested in holding the token = less selling pressure

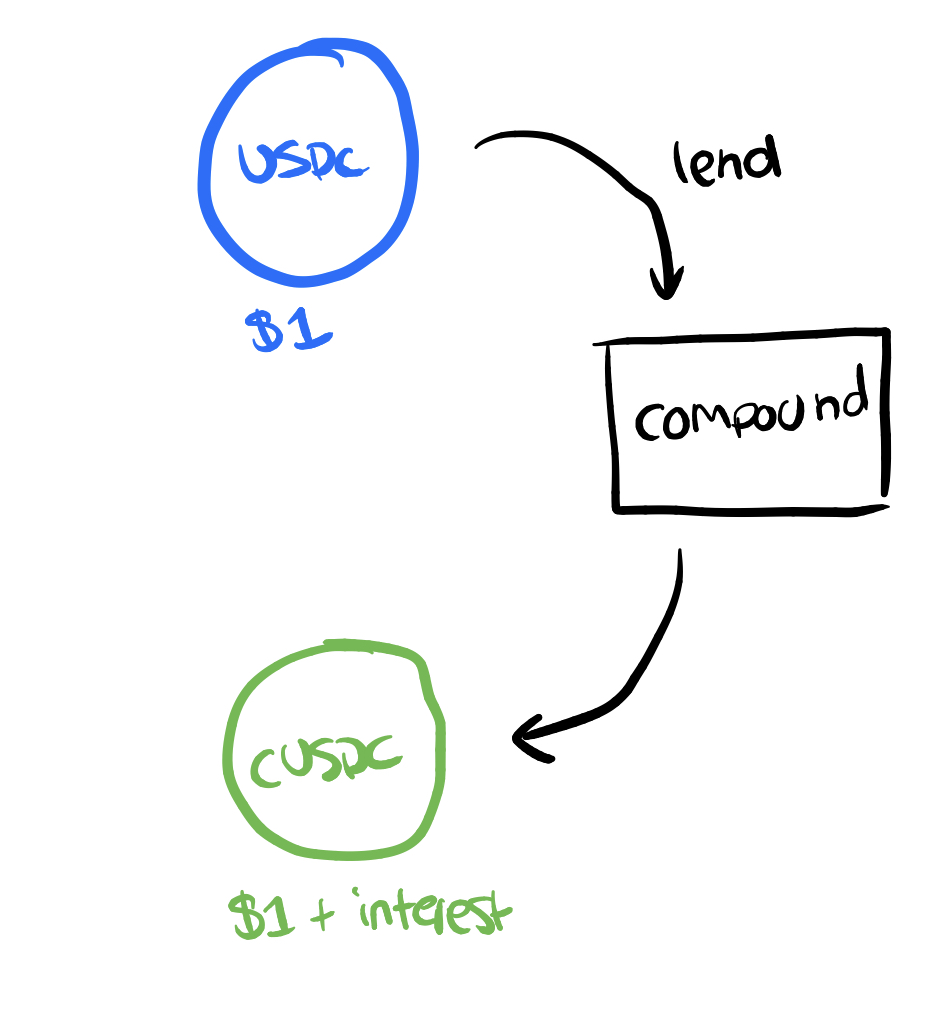

- xCVP would be a really good decentralized collateral on different websites like AAVE / Cream / Maker / Compound and in addition the user is still able to earn the underlaying protocol fees

- because of this “buyback” there is a constant buying pressure for CVP and that should increase the price of CVP in the long run

Specification:

It is possible to attract a complete new audience cause more users are interested in cash flows. Let me show you an example:

You mint an ASSY token and decide to LP (50% ETH / 50% ASSY) on balancer and stake it on the powerpool website. That means you have exposure to AAVE, SNX, SUSHY, YFI and ETH price action. I would call this not just an LP position, it is more like a whole and really good portfolio management if you believe in the DEFI space. You always have 50% ETH and 50% ASSY (including the DAMM mechanism which will change the composition of ASSY with the performance of the underlaying tokens). Additionally you earn yield of the staked ASSY components AND have the right to vote for the underlaying protocols.

On top of that you earn CVP because you stake it on the powerprotocol website (as long as the liquidity mining programm is working) and on top of that you earn the protocol fees of CVP when the vesting period has ended. And since Powerpool is not just an Index or ETF, it is an AMM that is integrated in1Inch right now, the fees that could be earned are much higher. Everything while having exposure to the underlaying tokens, votings rights and without any leverage position. In my mind, this is one of the most innovative projects in the whole defi space with a huge upside potential if we are able to offer a cashflow to the tokens holders.

And we should not forget the importance of the CVP voting rights. If the powerpool procotocl will hit the defi main stream every project should have exposure to CVP because the CVP voters have the rights to change the pools like PIPT, YETI, ASSY.

I really hope you like the idea of it. I sadly dont have the skills and the knowledge how further steps would look like. I really hope some of you really smart community members can think about this idea and find a way to improve it and find ways to increase the value of the powerpool protocol.

Many thanks for the time.

PS: This proposal does not include how the treasury should be allocated. This proposal is for a future distribution of the fees to stakers/holders.

And governance should be 100% retained even with xCVP.

And governance should be 100% retained even with xCVP.