My team and I have been watching the forums / discord recently and we’ve been really impressed by the level of engagement from the community so far. While there are a lot of factors still up in the air right now, we wanted to propose a comprehensive model that pulls everything together and charts a strong path forward for the community heading into mainnet launch. We’ve seen new projects fall out of favor and quickly lose traction after their unsustainable, unvested rewards dry up. We don’t want PowerPool to follow in their footsteps, but rather set a positive example with a sustainable, long-term oriented strategy.

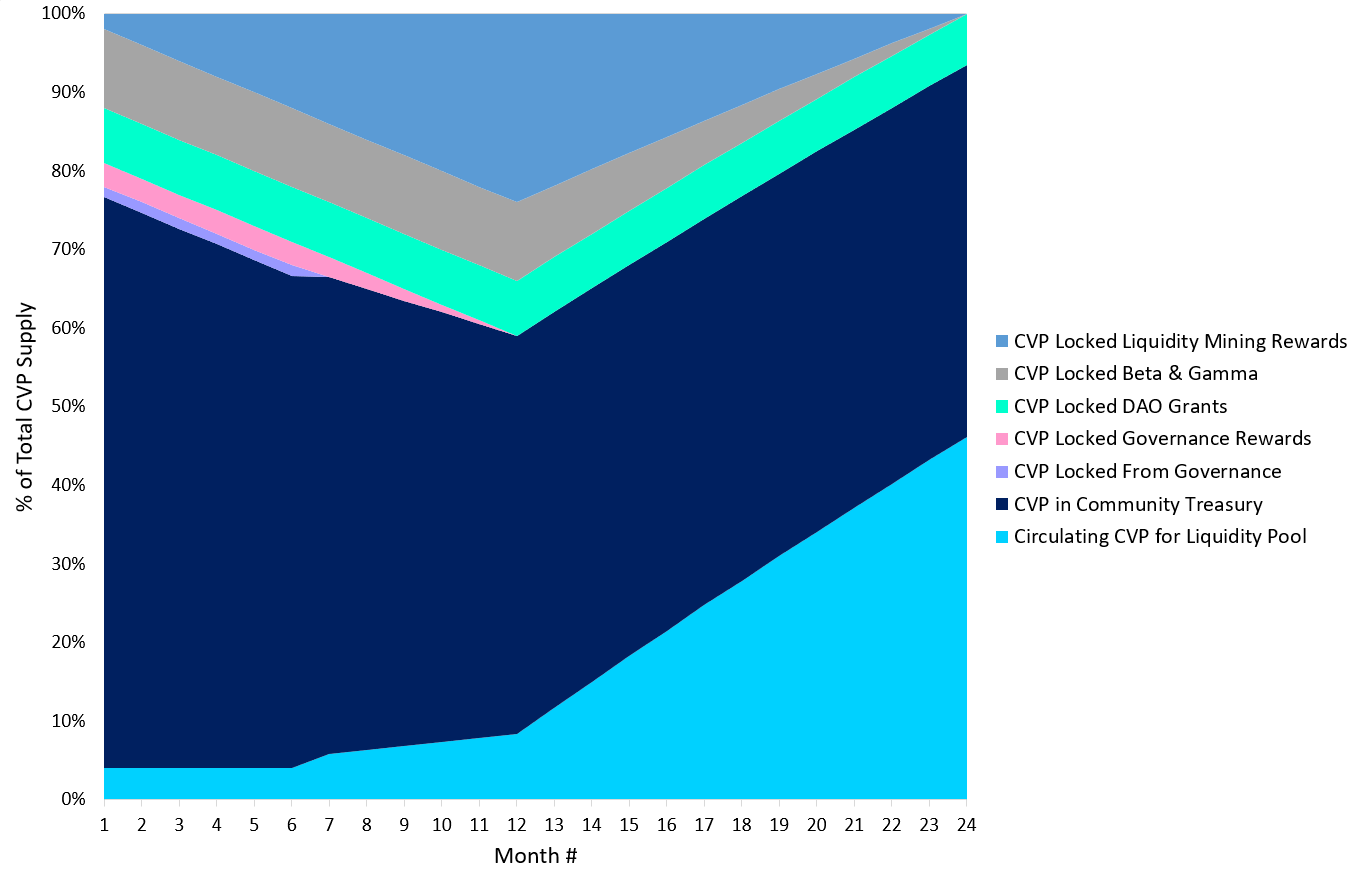

Currently, only 5,360,154 CVP are in circulation, with ~95% of the total supply still locked up / not distributed. Luckily, this gives us a lot of dry powder to work with in terms of optimizing the supply side release schedule and liquidity mining incentives for bootstrapping adoption. We propose the following:

- Beta (5m CVP) - 1 year lock then 12 month linear vest

- Gamma (5m CVP) - 1 year lock then 12 month linear vest

While this is a much longer time period than others have put forward, we believe it is the right decision. We need to do right by the current CVP holder base since they are comprised of either 1) Alpha participants who held, 2) people who purchased on the open market or 3) people who took risk providing liquidity. It would be a disadvantage to those early supporters to release the Beta and Gamma distributions quickly, given those participants did not take any risk. As Gamma participants ourselves, we are happy to accept this lock-up period because we believe it gives PowerPool the best chance to succeed.

- DAO Grants (7m CVP) - 2 year lock then 12 month linear vest

For PowerPool’s meta-governance to work, the CVP community needs to be on good terms with the DAOs of the composite members, operating to the mutual benefit of all. We believe allocating 7% of the total supply for DAO grants will align incentives between both communities and make admittance into the first PowerIndex more appealing. With this approach, PowerPool will hold the governance tokens of the composite members, while they hold the governance token of PowerPool itself. At current prices, this grant would be worth ~$2m for each DAO, however, as the TVL of the PowerIndex grows, so too will the value of the grant they hold. We propose the 2 year lock and 12 month linear vest so that the receiving DAOs have a long-term stake.

Combined, the lock ups above leave 77,639,846 CVP available for incentives. We believe this should be deposited into the community treasury for CVP stakers to govern. From that supply, we propose a liquidity mining program that distributes 2m CVP a month for the first year, with rewards locked for 1 year from the date they’re paid (similar to Synthetix’s program). Based on the attached model, we believe this will provide an attractive, yet consistent, yield for the initial bootstrapping phase without overpaying. Our goal is for the yield to rise from an increasing CVP price, not from a short-term supply dump (this is not financial advice). In case the 2m CVP a month ends up being too much or too little of an incentive, we suggest giving the community power to adjust the rewards distribution every month. With this plan in place, the community treasury will control ~50% of the total supply by the end of year 1. The community can vote to use that supply to liquidity mine a new PowerIndex or even burn it if they believe that is no longer necessary. (Everyone should DYOR and evaluate your risk tolerance before participating in liquidity mining).

We also propose allocating 3m CVP as a reward for the first vote to decide on the PowerPool’s composition. With a circulating supply 5,360,154 CVP this could be worthwhile. However, we should emphasize that participating in this first vote will lock up your CVP for 6 months, meaning those who participate won’t be able to use those same CVP to provide liquidity at the launch of the PowerIndex (although participants will still be able to use their locked CVP to vote on other proposals). The 3m CVP reward allocation will be locked for 6 months and vest linearly over the following 6 months. In our model, we forecast that 25% of the current circulating supply will participate and be locked up. While this may seem like a large reward, when we discuss the dynamics of the PowerIndex it will become clear why incentivizing the lock up of more CVP supply makes sense. Before we get into that, let’s summarize what this supply distribution could look like over the following 2 years.

As you can see in the chart above, this leads to a very tight supply side over the first year, with vested tokens gradually unlocking in year 2 after the initial bootstrapping phase is complete. Now let’s talk about what this means for the PowerIndex. When considering it’s design, we borrowed some concepts from another portfolio investment of ours - RUNE. In that design, as the value of exogenous assets in their pools rises, so does the value of RUNE based on their security model and incentive pendulum. The PowerIndex can affect CVP in a similar way. As the TVL of the PowerIndex rises, so too must the value of CVP held within it, given its minimum target weight of 1/8. For example, let’s say the TVL of the pool is $240m. That means CVP must represent at least $30m of that value. If the circulating supply of CVP is only 3m, then that equates to a price of a least $10 per CVP for the pool dynamics to work. This also creates a reflexive feedback loop.

As the TVL of PowerIndex rises > the value of CVP rises > the yield for providing liquidity scales with it

For this design to work, it hinges on the ability to re-direct incentives when CVP falls below its target weighting. If CVP < 1/8 of the TVL in PowerIndex, then incentives pivot to rewarding the liquidity providers who add more CVP to the pool, bringing the index back to its targeted equilibrium.

Previously, we proposed that trading fees from the PowerPool should be saved to create permanent liquidity and governance power for the CVP community, rather than being paid out to liquidity providers. As TVL rises and sustains itself over long periods of time, from the steady stream of incentives, more and more governance tokens will be earned from trading fees. The PowerIndex will certainly be the pool with the deepest liquidity for CVP, but it may also grow to be a spot of deep liquidity for its composite members as well. Traders could capitalize on the unique ability to trade between the top DeFi tokens without any intermediary pass-through asset. As liquidity deepens, slippage declines, further reinforcing the pool’s appeal to traders.

My partner Anil also came up with a great way to generate more permanent liquidity from fees, incentivize long-term oriented stakeholders and mitigate potential manipulation of the incentive pendulum detailed above. We suggest a withdrawal fee that decays over time. For example, let’s say you add liquidity to the pool then immediately want to withdraw those tokens. This would incur a penalty withdrawal fee of 10%. However, if you wait a month to withdraw, the fee declines to only 1%. These are placeholder numbers for now and will require more modeling to fine tune what that decaying withdrawal fee curve should look like. Will this deter liquidity from short-term oriented LPs? Yes, but in their absence rewards for long-term oriented LPs will increase, which is the stakeholder group we want to stick around.

This is a lot to consider but we encourage all members of the community to think it over, check out the model we’ve attached, ask questions and engage in discussion. We believe there’s a very unique opportunity here to liquidity mine a DeFi index with meta-governance coordinated on layer 2, uniting the communities and aligning the interests of the top protocols in the space. We’re happy to commit ourselves for the long-term, we hope you do as well.